Home Loan EMI Calculator

Calculate Your EMI

Article Insight: A $500,000 loan at 6.5% for 25 years costs $520,000 in interest alone. That's more than the home's original price.

Your Results

Monthly EMI

$0

Total Interest Paid

$0

Total Repayment

$0

If your EMI exceeds 35% of your take-home pay, you're in the red zone (as noted in the article).

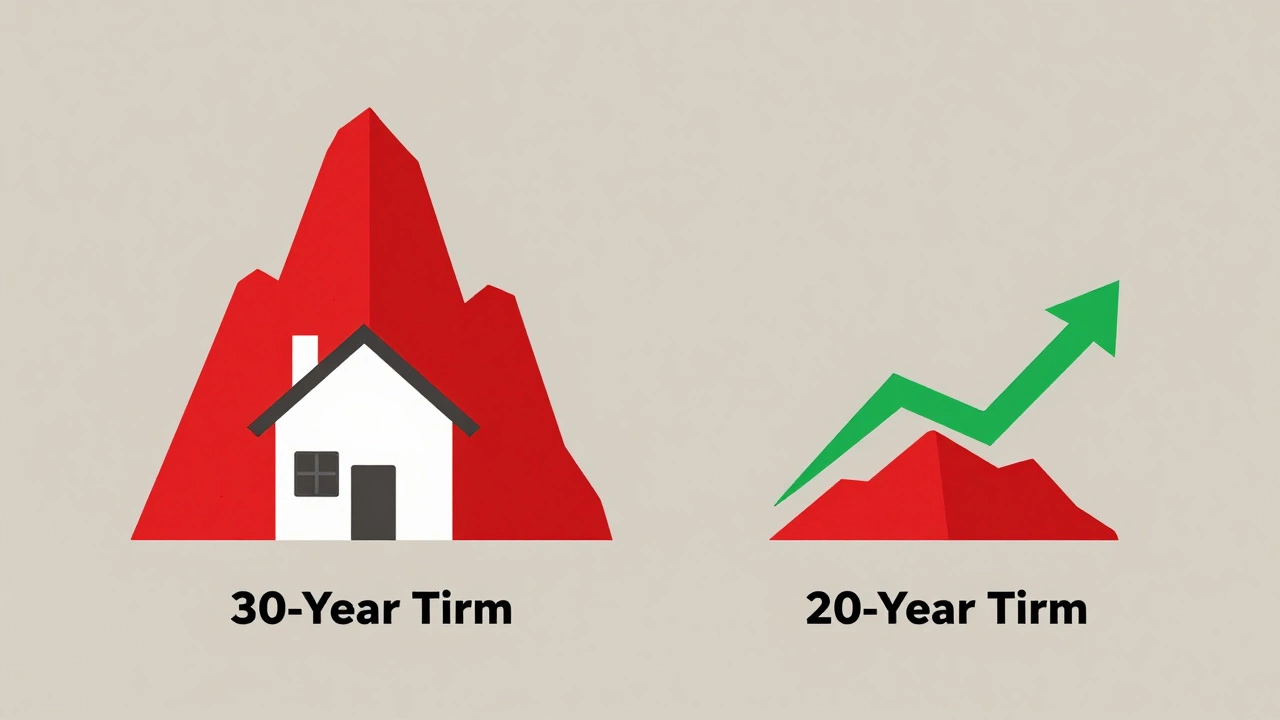

Impact of Shorter Term

A 20-year term instead of 25 years could save you $0 in interest.

When you see a house you love, the price tag might make you pause. But the real test isn’t the sticker price-it’s the monthly EMI. Is EMI costly? The answer isn’t yes or no. It’s EMI-and what you’re really paying for it.

What Exactly Are You Paying Each Month?

An EMI-Equated Monthly Installment-isn’t just your loan payment. It’s a mix of principal and interest, chopped up into neat monthly chunks. Most people think they’re only paying for the house. They’re not. They’re paying for the bank’s money over 15, 20, or even 30 years.

Take a $500,000 home loan at 6.5% interest over 25 years. Your EMI? Around $3,400. Sounds manageable. But here’s the catch: over that time, you’ll pay nearly $520,000 in interest alone. That’s more than the original loan. You’re not buying a house-you’re financing decades of interest.

That’s the hidden cost. Banks don’t advertise it. Real estate agents don’t mention it. But every EMI you pay after the first few years is mostly interest. In the first five years, you might pay just $80,000 toward the principal. The rest? Gone to the lender.

Why EMI Feels Affordable-Until It Doesn’t

EMIs are designed to feel easy. $3,000 a month? You can stretch to that. But life doesn’t stay still. Kids start school. Medical bills pop up. One parent loses a job. Interest rates rise. And suddenly, that ‘affordable’ EMI becomes a trap.

Here’s what most people don’t realize: EMI doesn’t change unless you refinance. Even if you earn more, your payment stays the same. But if your income drops, your EMI doesn’t drop with it. That’s the risk. You lock in a fixed number, but your life moves around it.

In Australia, over 40% of homeowners say their EMI eats up more than 35% of their take-home pay. That’s the red zone. At that level, one emergency can derail your finances. And if rates go up? You’re stuck. Unlike credit cards, you can’t just pay the minimum and hope for the best.

How Interest Turns Small Loans Into Big Bills

Interest compounds. That’s the math no one explains. A 1% rise in interest rate on a $600,000 loan over 30 years adds over $110,000 to your total repayment. That’s not a small tweak. That’s a new car. Or a year’s rent. Or your child’s university fees.

Let’s say you take a loan at 5.5% instead of 6.5%. Over 25 years, you save nearly $140,000. That’s not a ‘small difference.’ That’s the equivalent of a fully paid-off second car. But most people choose the lender with the lowest EMI, not the lowest total cost. They think they’re saving money. They’re not. They’re just delaying the pain.

Here’s a simple rule: If your EMI is under $2,500 for a $500,000 loan, you’re probably getting a bad deal. At today’s rates, that’s only possible with a 30-year term or a huge down payment. Anything shorter than 20 years with that loan size will push you past $3,000. And if you’re under 35, a 30-year term means you’ll still be paying when you’re 65.

EMI vs. Other Debt: Why Home Loans Are Different

People compare home loan EMIs to credit cards or car loans. That’s misleading. Credit cards charge 20%+ interest but you can pay them off in months. Car loans? Usually 5 years. Home loans? 25 to 30. That’s not a loan-it’s a financial commitment that outlasts most jobs.

And unlike credit cards, you can’t easily refinance. Banks make it hard. They charge fees. They demand new appraisals. They check your credit again. By the time you get a better rate, you’ve paid thousands in extra interest.

Worse, many Australians don’t realize their EMI includes insurance, property taxes, and strata fees. That’s not part of the loan-but it’s part of your monthly cost. You think you’re paying $3,200 for the loan. You’re really paying $3,800. And if your strata fees go up? No one adjusts your EMI. You absorb it.

When EMI Is Worth It-And When It’s Not

EMI isn’t always bad. If you’re buying in a growing area, your property could double in value. If you’re renting for $3,000 a month and your EMI is $2,800, you’re building equity. That’s smart.

But if you’re buying just because you think you ‘should,’ or because your friends are doing it, you’re in trouble. If your job is unstable, if you’re planning to move in 5 years, if you have high medical bills or kids in private school-then a long-term EMI is a gamble.

Here’s a quick test: Can you pay off your loan in 15 years if you doubled your EMI tomorrow? If not, you’re not ready. A 25-year term sounds safe. But it’s just a delay tactic. You’re not building wealth-you’re renting from the bank.

Some people think: ‘I’ll pay extra when I can.’ But most don’t. Studies show only 12% of Australians consistently make extra repayments. The rest get comfortable. Then life happens. And the debt stays.

How to Reduce the Cost of Your EMI

You can’t avoid EMI. But you can control how much it costs.

- Put down 20% or more. Avoid LMI (Lenders Mortgage Insurance). That’s a one-time fee, but it can be $15,000 or more. Paying more upfront cuts your loan and your interest.

- Choose a 20-year term. You’ll pay more per month, but you’ll save over $200,000 in interest on a $600,000 loan.

- Make extra payments. Even $200 extra a month cuts 5 years off your loan and saves $120,000.

- Refinance if rates drop 0.5% or more. Don’t wait for a 1% drop. That 0.5% could save you $80,000 over the life of the loan.

- Use an offset account. Every dollar in your offset account reduces your interest. If you have $10,000 saved, you’re effectively paying interest on $590,000, not $600,000.

And don’t fall for ‘interest-only’ deals. They sound great for the first 5 years. But then your EMI jumps 30-40%. You’ll be shocked. Most people can’t afford the new payment. They sell. Or they refinance into another trap.

What Happens If You Can’t Pay?

Defaulting on your EMI isn’t like missing a credit card payment. Banks don’t send reminders. They don’t give warnings. They start legal action. Within 3 months, they can list your home for auction. And you lose everything you’ve paid.

Even if you’re just one month late, your credit score takes a hit. That affects your ability to get a car loan, a credit card, or even a phone plan. Your EMI isn’t just a payment. It’s your financial lifeline.

That’s why emergency savings matter more than ever. You need at least 6 months of EMI in the bank. Not for vacations. Not for upgrades. For survival.

Final Thought: EMI Is a Tool. Not a Trap.

EMI isn’t costly by design. It’s costly because people don’t understand it. They focus on the monthly number. They ignore the total. They think ‘affordable’ means ‘safe.’ It doesn’t.

The real question isn’t ‘Is EMI costly?’ It’s ‘Are you prepared for what EMI really means?’

If you’ve done the math, built a buffer, and know your loan inside out-then EMI is a powerful tool. If you’re just going with the flow, hoping it works out-you’re already paying too much.

Is EMI always the best way to buy a home?

No. EMI is only the best option if you plan to stay in the home for at least 7-10 years, have stable income, and can afford higher payments to reduce interest. If you’re unsure about your job, planning to move soon, or can’t save for a 20% deposit, renting might be cheaper and safer.

Can I reduce my EMI without refinancing?

Yes. You can’t lower the monthly amount unless you refinance, but you can reduce the total cost by making extra payments. Even small amounts-like $100 or $200 extra per month-go straight to the principal and shrink your loan faster. This cuts interest and shortens your loan term without changing your EMI.

Why does my EMI stay the same even when interest rates drop?

Most home loans in Australia are fixed-rate for 1-5 years. After that, they switch to variable. If you’re on a fixed term, your EMI won’t change until the term ends. Even if the market rate drops, your bank isn’t required to lower your payment. You need to refinance to get a better rate.

How do I know if my EMI is too high?

If your EMI (including insurance and fees) takes up more than 30% of your take-home pay, it’s high. If it’s over 35%, you’re in danger. Use an EMI calculator to see your total repayment over the life of the loan. If the interest equals or exceeds the loan amount, your EMI is costing you more than the house.

Should I pay off my EMI early?

If you have no high-interest debt, no emergency fund, or no other investments with better returns, then yes. Paying off your home loan early is one of the safest financial moves you can make. It’s like earning a guaranteed return equal to your interest rate-often 5-7%. That’s better than most savings accounts or even some shares.

What to Do Next

Grab your latest home loan statement. Look at the interest paid last year. Now check your remaining balance. If the interest paid is more than 70% of your total payments, you’re still in the interest-heavy phase. That’s normal-but it’s also your chance to act.

Open an offset account if you don’t have one. Start saving $100 extra per month-even if it’s just from cutting coffee. Use an online EMI calculator to see how much you’d save by shortening your term to 20 years. Talk to a mortgage broker who works for you, not the bank.

EMI isn’t the enemy. Ignorance is. The moment you understand what you’re really paying, you stop being a borrower-and start being a homeowner.