If you invest $3000 today in a mutual fund in India, how much could it grow in 20 years? The answer isn’t a single number-it depends on where you put your money, how the market moves, and whether you stay patient. Many people think long-term investing is magic. It’s not. It’s math. And that math can work hard for you if you understand it.

What happens when you invest $3000 in mutual funds?

Let’s say you put $3000 into a mutual fund today. That’s your starting point. In 20 years, that money won’t just sit there. It’ll grow-or shrink-based on the fund’s annual return. The key word here is compound interest. It’s not just about earning returns. It’s about earning returns on your returns. That’s where real growth happens.

For example, if your fund averages 10% annual returns, $3000 becomes about $20,180 after 20 years. That’s more than six times your original money. But if returns are only 6%, you end up with $9,620. That’s still a solid gain, but it’s less than half of what you’d get at 10%. The difference? Over $10,000. That’s why choosing the right fund matters.

Historical returns of Indian mutual funds

India’s mutual fund industry has grown fast. Since 2000, equity mutual funds have delivered average annual returns between 10% and 14%. That’s not guaranteed, but it’s backed by data. The NSE Nifty 50 index, which many index funds track, returned about 12.5% per year from 2006 to 2025. That’s over 17x growth in 19 years.

Large-cap funds, like those tracking the Nifty 50, have consistently returned 11-13% annually over the last two decades. Mid-cap funds, which take more risk, have returned 13-15% on average-but with bigger ups and downs. If you pick a good mid-cap fund and hold it for 20 years, you might hit 14% returns. But you have to stick with it through crashes.

Debt funds? They’re safer. But they don’t grow as fast. A good corporate bond fund might return 7-8% annually. That turns $3000 into $12,000 over 20 years. Not bad, but it won’t beat inflation long-term. For real wealth building, equity is still king in India.

How to pick the right mutual fund

Not all mutual funds are made equal. You can’t just pick the one with the highest past returns. Past performance doesn’t guarantee future results. But it does show consistency. Look for funds that have beaten their benchmark for at least 10 years. That’s a real signal.

Check the expense ratio. A fund charging 2% fees eats away your returns. A 1% fee is better. A 0.5% index fund? Even better. For example, if two funds both return 12% before fees, but one charges 1.5% and the other 0.6%, the second one leaves you with 11.4% net. Over 20 years, that tiny difference adds up to over $4,000 extra.

Also, look at the fund house. HDFC Mutual Fund, ICICI Prudential, SBI Mutual Fund, and Axis Mutual Fund have been around for decades. They have strong track records, low churn, and clear strategies. Avoid funds that change managers every year. Stability matters.

Systematic Investment Plans (SIPs) beat lump sums

Most people don’t invest $3000 all at once. They save up. That’s where SIPs come in. Instead of putting $3000 in one go, you invest $125 every month for 20 years. That’s $30,000 total. But because you’re buying units at different prices over time, you reduce risk.

If the market averages 12% annual returns, your $125/month SIP becomes $118,000 in 20 years. That’s nearly 4x more than if you’d invested the lump sum. Why? Because SIPs let you buy more units when prices are low and fewer when they’re high. It’s automatic dollar-cost averaging.

And here’s the kicker: you don’t need to time the market. You just need to keep investing. Even if the market drops 30% in year 5, your SIP keeps buying. When it rebounds, you’re already holding more units than someone who waited for the bottom.

What if inflation eats your gains?

Some people say, “But inflation will ruin this.” True. India’s inflation has averaged 6% over the last 20 years. So if your fund returns 12%, your real gain is only 6%. That still means your money doubles in about 12 years.

But here’s the thing: inflation doesn’t just hurt-it helps. Wages rise. Prices rise. Companies earn more. That’s why equity funds grow. They own companies that adapt. A house that cost ₹20 lakh in 2006 costs ₹80 lakh today. But a mutual fund that grew at 12% would have turned ₹3000 into ₹20 lakh. That’s not just keeping up-it’s outpacing.

Debt funds and savings accounts? They struggle with inflation. A fixed deposit at 6.5% might earn you ₹3,000 in interest over a year, but if inflation is 6%, you’re only ahead by ₹50. That’s why long-term wealth needs equity exposure.

Real examples from Indian investors

Take Priya, 30, from Pune. She started a ₹25,000/month SIP (about $300) in a large-cap index fund in 2015. She didn’t touch it. In 2025, her account was worth ₹1.8 crore. That’s over $215,000. She invested ₹30 lakh total. Her money grew 6x.

Or Raj, 35, from Jaipur. He put ₹1.5 lakh ($1,800) into a mid-cap fund in 2018. The fund dropped 40% in 2020. He kept adding ₹5,000/month. By 2025, his ₹3 lakh investment was worth ₹8.2 lakh. That’s 2.7x growth, even after a crash.

These aren’t lucky stories. They’re repeatable. You don’t need to be rich. You just need to start early, stay consistent, and ignore the noise.

What if you stop investing early?

Time is your biggest advantage. If you invest $3000 at age 25 and stop after 5 years, your money could grow to $15,000 by 45. But if you wait until 35 to invest $3000 and stop after 5 years, you only get $9,000 by 55. Same money. Different outcome. Because the first one had 20 extra years of compounding.

That’s why starting early matters more than how much you put in. Even $100/month, started young, can beat a $10,000 lump sum started late.

Don’t panic during market crashes

Markets crash. Always have. In 2008, the Nifty fell 57%. In 2020, it dropped 38% in two months. If you sold then, you locked in losses. If you held-or kept investing-you gained everything back and more.

Between 2008 and 2025, the Nifty 50 rose 550%. People who sold in 2009 missed the biggest bull run in Indian history. If you’re investing for 20 years, short-term drops are just noise. Your goal isn’t to avoid losses. It’s to stay invested through them.

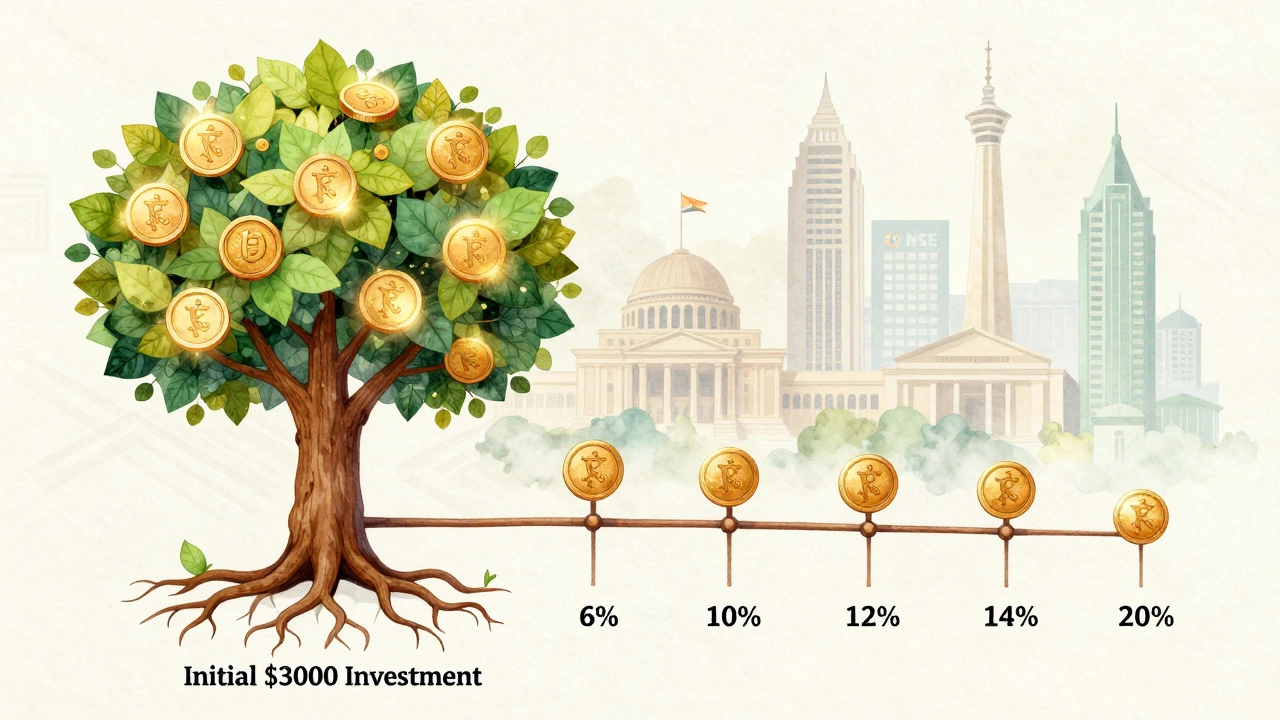

Final math: Your $3000 in 20 years

Let’s break it down:

- At 6% annual return: $3000 becomes $9,620

- At 8% annual return: $3000 becomes $14,000

- At 10% annual return: $3000 becomes $20,180

- At 12% annual return: $3000 becomes $28,980

- At 14% annual return: $3000 becomes $40,570

These numbers assume no additional investments. If you add $100/month on top of your $3000, you could easily double these results.

So, how much will $3000 be worth in 20 years? It depends. But if you invest wisely in Indian equity mutual funds and hold on, it could be anywhere from $10,000 to over $40,000. That’s not luck. That’s compound growth.

What to do next

Start today. Open a mutual fund account through a platform like Groww, Zerodha Coin, or Paytm Money. Pick a low-cost index fund or a large-cap fund with a 10-year track record. Set up a monthly SIP of $100-$200. Don’t check it every week. Don’t move it when the news is scary. Just let it grow.

Twenty years sounds far off. But right now, your $3000 is already on its way.

Can I really grow $3000 to $40,000 in 20 years with mutual funds in India?

Yes, if you invest in equity mutual funds that deliver 12-14% annual returns. Historical data shows that Indian equity funds, especially large-cap and index funds, have averaged 11-14% over the last 20 years. Compounded over two decades, $3000 grows to over $40,000. But this only happens if you stay invested and don’t panic during market drops.

Is it better to invest $3000 all at once or in monthly SIPs?

For most people, SIPs are better. Investing $3000 in one go exposes you to market timing risk. If you invest on a market high, you could lose 20-30% in the next year. SIPs spread your investment over time, lowering your average cost. Over 20 years, a $125/month SIP can grow to over $118,000 at 12% returns-far more than a one-time $3000 investment.

Which mutual funds in India have the best long-term returns?

Top performers over the last 10-15 years include Nippon India Index Fund (Nifty 50), HDFC Index Fund, ICICI Prudential Bluechip, and SBI Bluechip Fund. These are large-cap funds with low expense ratios (under 0.5%) and consistent outperformance. Avoid small-cap or thematic funds unless you understand the risk. Stick to diversified equity funds with long track records.

How does inflation affect mutual fund returns?

Inflation doesn’t erase equity returns-it’s built into them. Companies grow, prices rise, and profits increase. If a mutual fund returns 12% and inflation is 6%, your real gain is 6%. That’s still strong. Debt funds and fixed deposits often return less than inflation over time, which means you’re losing buying power. Equity mutual funds are one of the few tools that reliably outpace inflation in India.

Should I invest in mutual funds or direct stocks?

For most people, mutual funds are easier and safer. Picking individual stocks requires time, research, and emotional discipline. You need to track company earnings, sector trends, and valuations. Mutual funds do that for you. A fund manager handles diversification, rebalancing, and risk. Unless you’re willing to spend 10+ hours a week learning stocks, mutual funds are the smarter choice.