GST Input Tax Credit Eligibility Checker

Expense Details

Result

Enter expense details and click 'Check Eligibility' to see if you can claim Input Tax Credit.

You just bought a new laptop. It’s for your business, but you also plan to watch movies on it this weekend. When you look at the invoice, there’s a chunk of money listed as Goods and Services Tax (GST). Your instinct might be to add that tax amount to your company’s books and claim it back as an expense. After all, the computer helps you work, right?

Here is the hard truth: In most cases, you cannot claim GST on goods or services used primarily for personal purposes. The Indian government has strict rules about what qualifies for Input Tax Credit (ITC). Mixing personal and business expenses without clear separation can lead to rejected returns, penalties, and even audits during your annual GST filing process.

The Golden Rule: Business Use Only

To understand why personal claims are risky, we need to look at Section 17(5) of the Central Goods and Services Tax Act, 2017. This section acts as a negative list. It explicitly blocks ITC for specific categories of goods and services.

The core principle is simple: GST is a tax on consumption. If you consume the good or service for yourself, your family, or non-business activities, the state does not allow you to reverse that tax. The logic is that businesses should only recover taxes paid on inputs that go into producing taxable outputs. If the output is 'personal enjoyment,' there is no taxable supply to offset against.

- Food and beverages: You cannot claim GST on lunch, dinner, or coffee unless it is part of a corporate event with specific documentation.

- Personal grooming: Haircuts, spa treatments, and cosmetics are strictly personal.

- Recreation: Gym memberships, movie tickets, and holiday bookings are off-limits.

If you try to claim these in your GSTR-3B return, the mismatch will show up when you reconcile with GSTR-2A (the auto-drafted purchase register). The supplier has declared they sold it to you, but if the nature of the purchase is clearly personal, the tax department flags it as ineligible ITC.

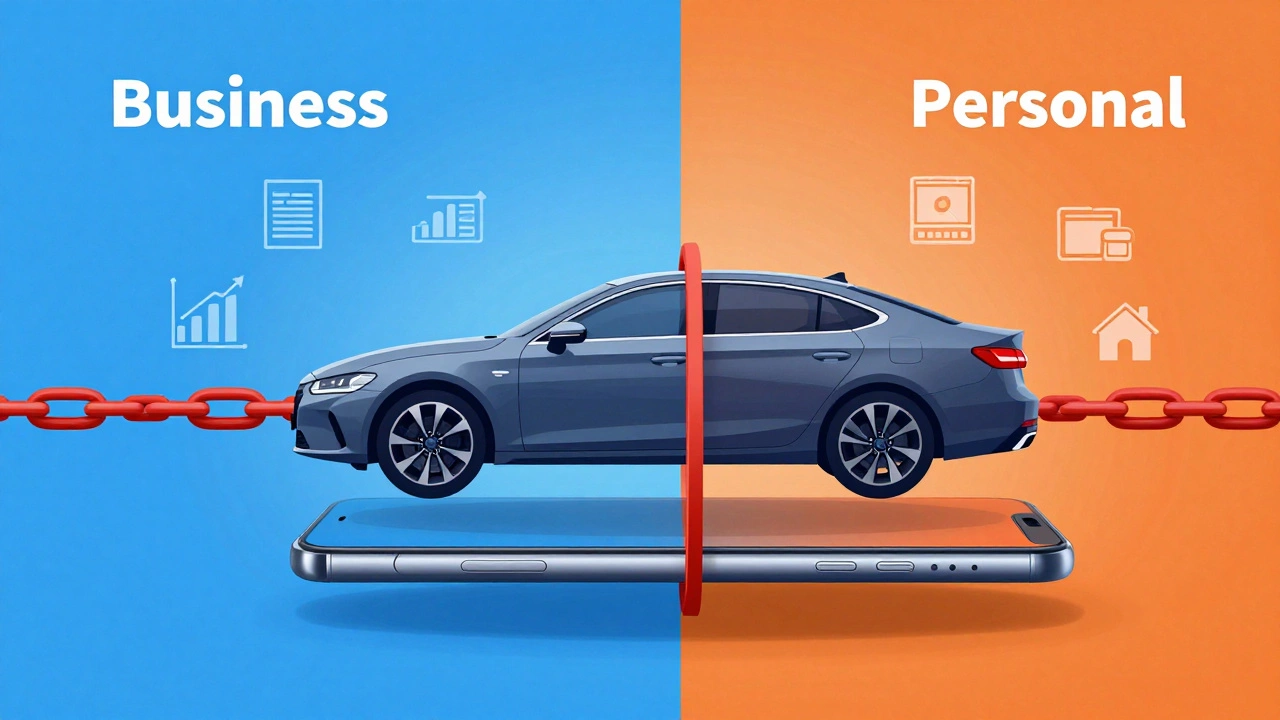

The Grey Area: Mixed-Use Assets

Things get trickier when an asset serves both purposes. Think about a car, a smartphone, or a high-end laptop. These items often cross the line between professional tool and personal luxury. How do you handle the GST on these?

The law requires you to determine the percentage of business use. However, for certain assets, the rule is binary. For example, passenger vehicles are generally blocked from ITC unless they are used for:

- Providing training in driving.

- Transportation of passengers (like a taxi service).

- Transportation of goods.

If you buy a sedan for your consulting firm and drive it home every day, you cannot claim the full GST. In fact, for most standard passenger cars, the entire ITC is blocked under Section 17(5)(a). There is no 'partial' claim allowed for typical commuter vehicles. You must pay the full tax out of pocket.

For electronics like laptops, the situation is slightly more flexible but still demanding. If the device is exclusively for business operations, you can claim the ITC. But if you use it heavily for personal gaming or streaming, auditors may argue that a significant portion is personal. To stay safe, maintain a log of business usage or ensure the device is issued to an employee solely for work functions.

Services vs. Goods: Different Rules Apply

There is a distinct difference between claiming GST on physical goods versus services. While goods have tangible ownership, services are consumed immediately. This makes personal use of services easier to identify and reject.

Consider office rent. If you rent a co-working space and use it 100% for business, you can claim the ITC. But if you rent a property that serves as both your home and office, you face a complex calculation. You must apportion the ITC based on the area used for business versus residential purposes. Documentation here is critical. Without floor plans and usage logs, the entire claim could be disallowed.

Another common trap is internet and telephone bills. Many freelancers and small business owners run their home internet through their company account. Since the bill comes in one lump sum, claiming the full GST is risky. A safer approach is to estimate the business usage percentage (e.g., 60%) and claim only that fraction of the ITC. Keep records ready to justify this ratio if questioned.

Consequences of Wrongful Claims

Why take the risk? The penalty structure for incorrect ITC claims is severe. Under the CGST Act, if you claim credit wrongly, you must reverse it along with interest at 18% per annum. This interest runs from the date the credit was originally availed until the date of payment.

Furthermore, if the tax officer determines that the wrongful claim was intentional to evade tax, it falls under fraud. Penalties can range from 10% to 100% of the tax evaded. In serious cases, criminal proceedings can be initiated. For a small business, this financial hit can be devastating.

Audits are becoming more data-driven. The GST Network (GSTN) uses AI tools to match supplier declarations with buyer claims. If your pattern shows consistent claims on categories typically associated with personal use-like dining, travel, or entertainment-the system flags your account for scrutiny. You don’t need a physical visit to get caught; digital reconciliation often reveals discrepancies automatically.

How to Stay Compliant

Avoiding trouble starts with clear internal policies. Here is how you can manage GST claims effectively:

- Separate Accounts: Keep personal and business bank accounts distinct. Pay business expenses from the business account only.

- Invoices Matter: Ensure every invoice has a valid GSTIN. No invoice means no ITC, regardless of usage.

- Maintain Usage Logs: For mixed-use assets, keep a simple record of how much time or capacity is dedicated to business.

- Review Section 17(5): Regularly check the updated list of blocked credits. The government occasionally amends this list, so staying informed prevents accidental errors.

If you are unsure about a specific expense, consult a Chartered Accountant before filing. It is cheaper to pay for advice than to pay penalties later.

| Expense Type | Eligible for ITC? | Conditions/Notes |

|---|---|---|

| Laptop/Computer | Yes (Conditional) | Must be used for business. High scrutiny if used for personal entertainment. |

| Passenger Car | No | Blocked under Section 17(5)(a) unless used for driving training or transport business. |

| Office Internet Bill | Yes (Partial) | Apportionment required if used for personal purposes at home. |

| Business Lunch | No | Food and beverages are generally blocked unless provided as part of employee welfare in specific contexts. |

| Gym Membership | No | Strictly personal recreation. |

Frequently Asked Questions

Can I claim GST on my mobile phone if I use it for work calls?

Generally, no. Mobile phones are considered personal accessories unless they are specifically issued by the employer for official communication and tracked via company logs. Even then, the claim is subject to strict scrutiny. Most individuals should treat mobile phone GST as a personal expense.

What happens if I accidentally claim GST on a personal expense?

You must reverse the credit in your next return. You will also need to pay interest at 18% per annum on the amount wrongly claimed. If the error is discovered during an audit, additional penalties may apply depending on whether it was deemed negligent or intentional.

Is there any exception for food and beverage expenses?

Yes, but limited. ITC on food and beverages is blocked unless it is supplied to employees as part of their employment benefits (like canteen services) or if it is part of a business promotion where the service is taxable. Standard client dinners or personal meals do not qualify.

Can I claim GST on travel expenses for a vacation?

No. Travel expenses for leisure, tourism, or personal vacations are completely ineligible for ITC. Only travel directly related to business meetings, site visits, or conferences can be claimed, and even then, proper documentation like meeting agendas is required.

How do I calculate partial ITC for mixed-use items?

You must determine the percentage of business use based on reasonable criteria such as floor area (for rent) or time logs (for equipment). Multiply the total GST paid by this percentage. Keep detailed records to support your calculation in case of an audit.