Indian Bank Account Opening: What You Need to Know Before You Start

When you start the process of Indian bank account opening, the formal process of setting up a savings or current account with a bank in India, often requiring identity proof, address verification, and tax documentation. Also known as bank account registration in India, it’s the first step to managing your money safely, earning interest, and accessing digital services like UPI and net banking. It’s not just about walking into a branch and filling forms. The type of account you open—whether it’s a regular savings account, an NRI account, or a zero-balance account—changes everything from interest rates to tax rules.

Many people don’t realize that savings account, a basic bank account designed for individuals to save money and earn interest, often with withdrawal limits and minimal fees. Also known as deposit account, it is the most common starting point for Indian residents isn’t the same everywhere. Some banks offer zero-balance accounts with no monthly charges, while others charge fees if you don’t keep a minimum balance. High-yield savings accounts exist too, but they often come with conditions—like requiring a certain number of transactions or limiting withdrawals. If you’re an NRI bank account, a special type of account offered to Non-Resident Indians, including NRE and NRO accounts, to manage income earned abroad or in India. Also known as NRI banking, it allows NRIs to hold foreign currency or Indian rupees with tax advantages, your options are different. You can’t just open a regular account—you need an NRE or NRO account to avoid tax traps and keep your money accessible. And if you’re planning to move back to India, how long you stay affects your tax status, which ties directly to how you manage your accounts.

Then there’s the digital side. online banking India, the use of internet-based services to perform banking tasks like fund transfers, bill payments, and account monitoring without visiting a branch. Also known as internet banking, it’s now the norm, not the exception. Most banks let you open an account online in under 15 minutes, but you still need to verify your identity through video KYC or physical documents. And don’t ignore bank fees India, charges applied by banks for services like ATM usage, account maintenance, cheque books, or fund transfers. Also known as bank charges, these can eat into your savings if you’re not careful. A no-frills account might seem cheap, but hidden fees for SMS alerts or failed transactions can add up fast.

What you find below is a collection of real, practical guides that cut through the noise. You’ll see what high-yield savings accounts really cost, how NRIs avoid tax mistakes, why some accounts are better than others, and how to avoid common traps when setting up your first account. There’s no fluff—just what works for people living in India, working abroad, or trying to build wealth without getting buried in paperwork.

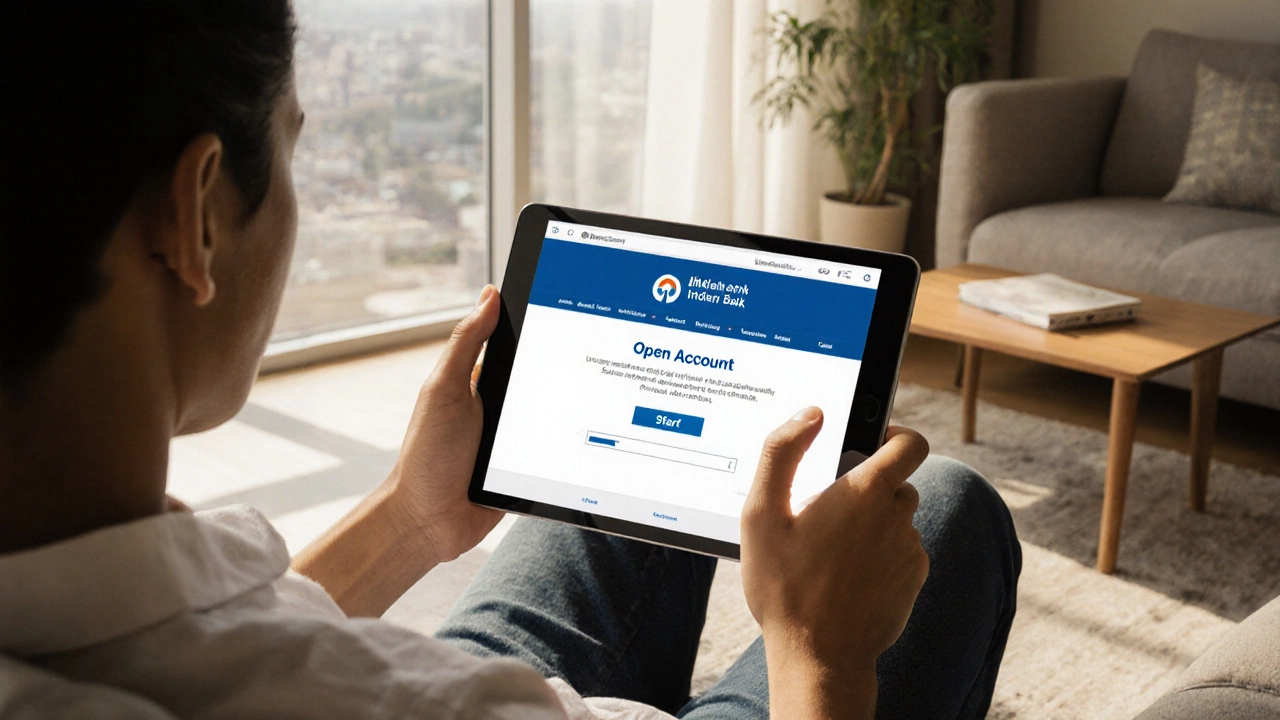

How to Open an Indian Bank Account Online - Step‑by‑Step Guide 2025

A step‑by‑step guide showing how to open an Indian Bank account online in 2025, covering required documents, the eKYC flow, funding options, common errors and security tips.

View more